William Stopford

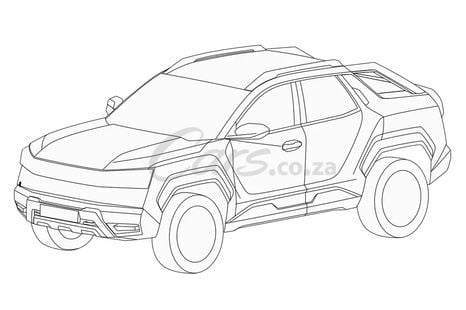

2027 LDV T60 nears Australia with tougher styling, more powerful engine

LDV Australia looks set to continue offering the cheaper T60 alongside its bigger, newer Terron 9, with an updated model firming for our market.

9 Hours Ago

The overall car market grew in 2021, but what were the five fastest-growing major brands? And which ones struggled on a volume basis?

News Editor

News Editor

Car makers with the highest-percentage sales increases and decreases over 2021 were mostly predictable enough to industry followers, though there were a few surprises.

Most brands avoided going backwards in 2021 as the overall market grew 14.5 per cent – even as COVID and semiconductor-related supply issues gripped the industry. Sales aren’t back to all-time high levels yet, but they’re trending up.

From the top 30 highest-volume brands, for example, only two posted a decline compared to the previous year. But while some merely bounced back, others had bumper performances. And a small list went backwards.

MORE: Australia’s 2021 new car sales detailed in full

Great Wall Motor isn’t the company it was, even five years ago, with the factory-run local subsidiary now its top export market.

The first Chinese auto maker to make an impact in Australia kicked off back in 2009 under a contracted distributor with budget utes and SUVs, only for sales to completely collapse several years later.

This applies double for its Haval SUV brand, which arrived here in 2016 to little fanfare but is now proving a force.

The new H6 and Jolion are proving more popular than their predecessors (the previous H6 and the H2 respectively) by far.

H6 sales were up 279.8 per cent, driven by the arrival of the new generation in April 2021, while Jolion sales were up 104.67 per cent on the H2’s 2020 tally.

Even the H9 managed to post a big increase (55.6 per cent, albeit to 543 sales) for 2021 before being discontinued.

]Then there’s the GWM Ute, which is vastly more desirable to shoppers than the old Steed – with 6906 sales in 2021, it was up 277 per cent on the Steed’s 2020 tally.

Genesis finally had SUVs to sell plus a much larger retail network, so it’s no surprise the upstart Korean luxury brand has managed to grow considerably.

The company said in August 2021 it expected to triple its 2020 sales and it actually managed to do slightly better, with 734 sales compared to 229 the year before. That pushed it past Alfa Romeo (618), though still a fair way off matching Jaguar (1222).

The GV80 introduced in October 2020 accounted for 287 of those sales, with the GV70 introduced in July 2021 accounting for 317. Genesis’ sedans didn’t fare as well, with the G70 down 34.7 per cent to 77 and the G80 down 10.2 per cent to 53.

Chinese brand MG had yet another cracking year, cementing itself in the top 10 with 39,025 sales. That put it ninth overall, above Subaru (37,015), Isuzu Ute (35,735), Mercedes-Benz (33,034), BMW (24,891) and GWM Haval (18,384).

The HS has resonated with Australian buyers in a way the old GS never did, with sales up 162.6 per cent to 6828. The MG 3 is firmly ensconced as Australia’s best-selling light car, up 92.4 per cent to 13,774 sales – that’s almost three times as many sales as the next best-selling, the Kia Rio (5644).

Finally the ZS family – consisting of the price-leader ZS, plus the ZS EV and ZST with many more safety features – was up 235.3 per cent. That gave MG yet another segment leader, fending off the stalwart Mitsubishi ASX in the small SUV segment (18,423 vs. 14,764).

It was a tumultuous year for SsangYong, which entered 2021 in bankruptcy protection after its parent Mahindra announced in 2020 it would no longer fund the Korean automaker.

By year’s end, however, SsangYong looked to finally have a saviour (or, at least, another short-term parent) in Korean bus manufacturer Edison Motor.

If the general public was aware of SsangYong’s travails, it didn’t affect sales much. Despite the loss of the small Tivoli SUV in 2020, the brand increased its sales from 1751 to 2978 sales in 2021.

That was still well adrift of fellow challenger brands GWM Haval and LDV, but its entire line-up was up. The Korando was up 40.1 per cent to 353 sales, the Musso up 73.7 per cent to 1883 sales, and the Rexton up 129.7 per cent to 742 sales.

LDV is another (formerly) British brand that was acquired by China’s SAIC Motor, though its lineup consists primarily of commercial vehicles.

Despite this, the D90 SUV was the biggest winner of the line-up with a percentage increase of 120.4 per cent over its 2020 tally, bringing it to 1576 sales.

The G10 people mover and van ranges were up 46.8 and 103.2 per cent, respectively, to 1064 and 3306 sales.

The T60 ute was up a comparatively modest 20.1 per cent to 6705 sales, though the arrival of a facelifted and more powerful version late in 2021 should boost sales further in 2022.

Finally, the antediluvian V80 van also grew its sales by 7.8 per cent, logging 553 sales overall.

LDV’s overall percentage increase only narrowly exceeded that of Isuzu Ute, a much higher volume brand – 35,735 sales versus 15,188 – which managed to increase its sales by 61.6 per cent over 2020.

Overall, 2021 was a good year for car brands in Australia. There were a handful of brands, however, that managed to go backwards.

Honda said publicly it expected its sales volumes to decline with the switch to an agency sales model focused on higher specification grades, but the fact is, its 39.5 per cent drop in 2021 is by far the biggest decline in the industry.

In addition to selling cars at set prices, it has also shrunk its retail network somewhat and winnowed down its model range considerably.

The affordable City and Jazz and ultra low-volume NSX were axed in 2020, with the Civic sedan following in 2021. Honda closed out the year by introducing a new generation of Civic, but only in a single, high-spec trim level.

Brand sales under the new business model were expected to drop to 1650 cars per month – or just shy of 20,000 sales per year. Honda ended up closing out the year with 17,562 sales, with every model bar the moribund Odyssey down on its 2020 tally.

The low-volume Accord declined by 45.5 per cent to 90 sales, the Civic by 59 per cent to 2950 sales, the CR-V by 27.8 per cent to 6875 sales, and the soon-to-be replaced HR-V by 25.8 per cent to 6069 sales.

Stellantis subsidiary FCA Australia announced in November 2021 it was withdrawing the Chrysler brand from Australia, 25 years after it had returned Down Under.

Though Stellantis has committed to its future, announcing this week it’s turning it into an electric vehicle-only brand by 2028, it currently sells only two models – the Voyager/Pacifica people mover and the 300 sedan – in only a handful of markets.

In Australia, its range was even more limited, offering only the 300. With production of the large sedan set to end before 2025, FCA Australia opted to withdraw the 300 sooner.

In its final year, sales were down to just 170 units.

The 300 was the only car in its VFACTS segment, which means the Upper Large < $100k segment – once home to models like the Ford Fairlane/LTD, Holden Statesman/Caprice and SsangYong Chairman – will be retired.

With Giulietta stock exhausted and the 4C running out, the Alfa Romeo brand is down to just two models: the Giulia and Stelvio.

One had a good 2021, the other had a bad 2021. Giulia sales were up 67.4 per cent year-to-date to 323, but this was effectively cancelled out by the Stelvio’s 53.6 per cent drop to 192 plus the loss of the Giulietta.

The Giulia managed to outsell the Jaguar XE (144) and Volvo S60 (168), but the Stelvio was effectively dead last in its segment. In a market clamouring for mid-sized SUVs, that’s a worrying sign, though Alfa Romeo did roll out a revised Stelvio range mid-year. Let’s see if it can improve its fortunes in 2022.

How did Citroen fare in 2021? Well, it was outsold by Ferrari for the second year in a row, which should tell you all you need to know.

With 175 sales, it managed to fend off Aston Martin (140) and Lamborghini (131), but we’re talking about a bread-and-butter brand in Europe that’s getting outsold by high-end exotic brands in Australia.

And its corporate cousin Peugeot, often dismissed as a niche brand itself, managed to log 2805 sales in 2021.

The C3 light hatch was up a lofty 87.2 per cent to 88 sales, albeit from a very low base.

The C4 arrived too late to make much of a difference, the C3 Aircross was effectively a dead man walking into 2021, and the C5 Aircross was Australia’s least favourite mid-sized SUV with just 58 sales – ok, the Hyundai Nexo logged 26 sales, but beating a hydrogen fuel-cell vehicle is nothing to crow about.

With the C4 now in Citroen showrooms nationwide and the C5 X set to join it later in 2022, the brand will have its largest line-up in Australia since 2016. We don’t expect it to storm up the sales charts, but let’s see if it can at least beat Ferrari in 2022.

Perhaps the only surprise on this list of the biggest losers in 2021 is Mercedes-Benz.

Mercedes-Benz Cars was down only 3.8 per cent, but Mercedes-Benz Vans dropped by 30.9 per cent.

While the Nissan Navara-based X-Class ute was never a big seller, its discontinuation was a blow for Mercedes-Benz Vans’ sales numbers, which dropped from 6778 in 2020 to 4686 in 2021. The volume-selling Vito was also down 16.7 per cent to 996 sales, though the more popular Sprinter van was up 24.2 per cent to 2997 sales.

Mercedes-Benz Cars’ sales figures were a mixed bag, and best observed through the lens of a horrible year for supply chains industry-wide. The popular A-Class and its CLA and GLA cousins were down 37.3, 37.6 per cent and 17.3 per cent, respectively, though the related GLB soared 272.1 per cent.

The GLC Coupe and Wagon were down 42.0 and 23.2 per cent, respectively, but Mercedes-Benz’s larger SUVs performed better. That included the G-Class (up 120 per cent), GLE Coupe (up 175.7 per cent), GLE Wagon (up 25.8 per cent) and GLS (up 36.5 per cent).

Still, though the car and SUV division performed better than the commercial vehicle division, the 3.8 per cent drop was still a worse outcome than BMW (up 5.8 per cent) and Audi (essentially flat, at 0.9 per cent)

William Stopford is an automotive journalist with a passion for mainstream cars, automotive history and overseas auto markets.

William Stopford

9 Hours Ago

William Stopford

10 Hours Ago

Damion Smy

13 Hours Ago

William Stopford

13 Hours Ago

William Stopford

16 Hours Ago

Ben Zachariah

18 Hours Ago

Add CarExpert as a Preferred Source on Google so your search results prioritise writing by actual experts, not AI.