James Wong

2026 Honda HR-V review

The Honda HR-V is a solid option in the small SUV segment, but there are some cons to go with its many pros.

56 Minutes Ago

Founder

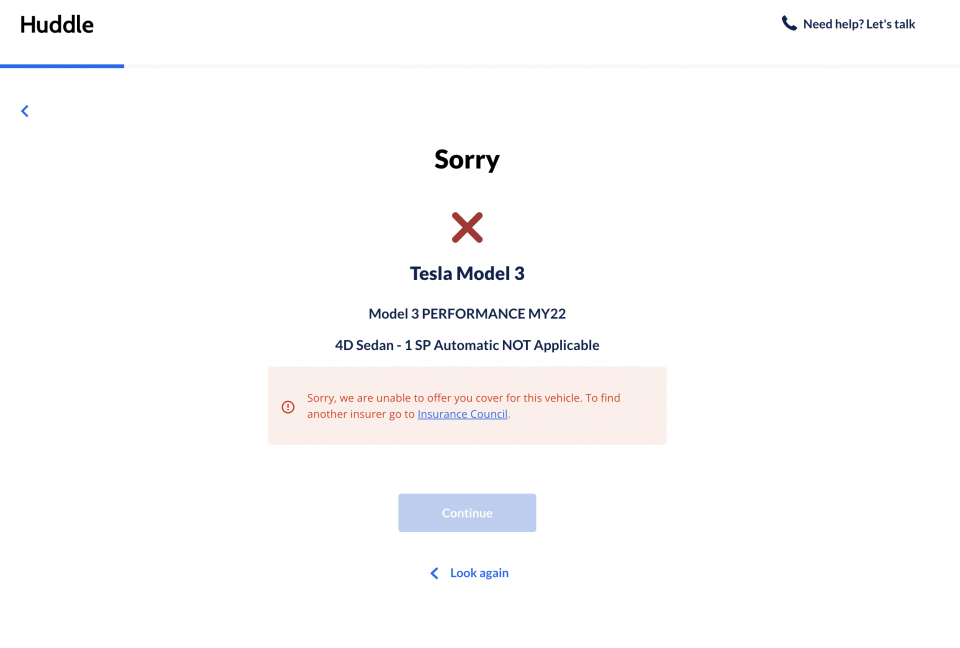

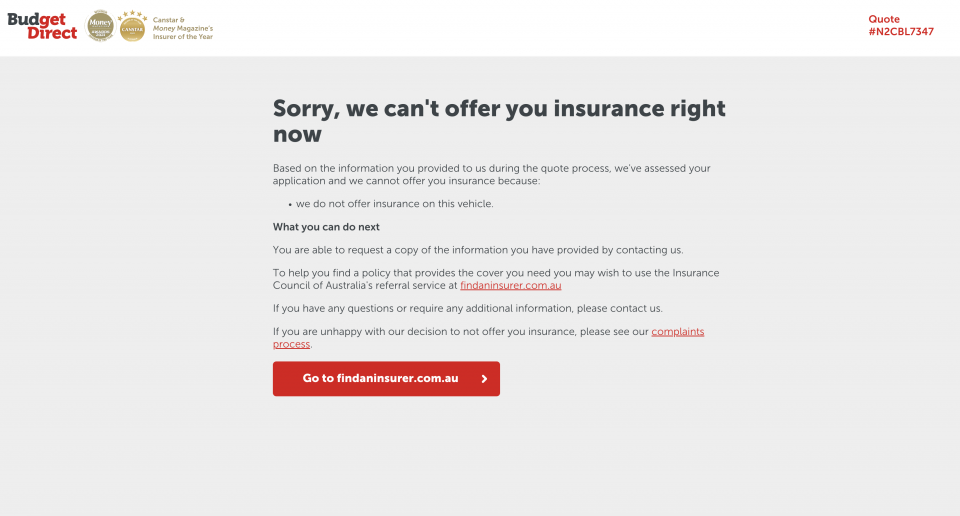

We’ve owned our Tesla Model 3 since November 2019. Each year when it comes time to renew our insurance policy, there’s a nasty surprise with a big jump in the premium or a total refusal to insure the vehicle entirely.

I was curious why it was so hard to get insurance for a Tesla… so I reached out to the Insurance Council of Australia to see why insurers refused to insure it, or charged much higher than an equivalently priced vehicle.

Before we get on to the why, I want to explain the situation we had with our Model 3. I’m over 30 years old, as is my wife. We haven’t had any insurance claims previously, we live just outside the Melbourne CBD, and neither of us has any licence issues.

Our first insurance policy in November 2019 was with UbiCar. It was for an agreed value of $96,800 (they also offered a new-for-old replacement) and the yearly premium was just over $1400. I thought that was a pretty reasonable price, so we locked it in and were pretty happy.

At this point the Model 3 was new to Australia and UbiCar was one of the few insurers that had it listed. They also required the driver to run an OBD monitor or phone app to track your driving performance.

As a reference, around the same time I bought my Toyota Supra. It was around $10,000 more expensive to purchase and I insured it with UbiCar as well, but it was for $1100 with an agreed value of $104,000.

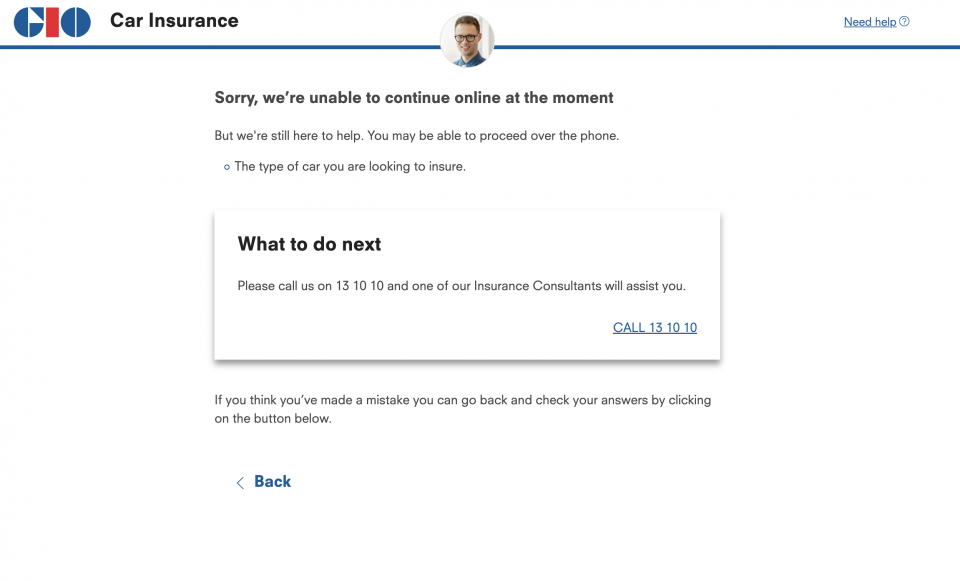

The following year is when things started to get expensive. UbiCar went out of business and I started shopping around, and noticed a number of insurers refused to offer any coverage, not even an expensive policy. Allianz even came in with a comical premium of $9000 for comprehensive insurance.

I ended up settling on AAMI, which came in at $1800 for comprehensive with limited mileage, a higher excess of $1100, and a lower agreed value of $80,000.

The following year is when things started to get a little crazy. In November 2021 when I received my renewal notice from AAMI it had jumped to just over $2000, and the agreed value dropped to $74,000.

So I went on the hunt for other quotes. I started pulling my hair out when some of the biggest insurers simply refused to offer insurance for a Tesla. The list of insurers that refuse to insure a Tesla include:

Even when I did find an insurer to eventually insure my car, the cost of the premium was equal to a car worth 50 per cent more than the Tesla, so it was proportionally much higher than an equivalently priced vehicle.

So what’s the story? I contacted the Insurance Council of Australia, and a spokesperson explained why Tesla and electric vehicles in general are so hard to insure.

“There are several reasons that may underpin the cost of insurance premiums,” they said.

“These may include:

While the first couple of reasons make sense, it’s the rest of them that are likely to take longer (and be more frustrating) to get on top of.

Many established premium brands in Australia carry large stockpiles of spare parts and some even run their own repair centres, so it’s less of a headache for insurers.

Tesla on the other hand seems to dish most of this out to the aftermarket, which appears to result in claims taking forever and becoming too complicated for insurers to deal with.

For example, when our Model 3 was delivered it had a paint defect. Tesla had to engage a third-party panel shop to repair the panel instead of performing this work in-house.

With Tesla now leading the charge on electric vehicle sales in Australia and more sales likely to come as a result of Model Y going on sale later this year, it’s a problem that will only compound as time goes on.

What’s the solution? Tesla runs its own insurance company in the USA that helps reduce the cost of premiums based on their in-house risk factors. That insurance isn’t available in Australia and there’s no indication of whether it will eventually be available.

Tesla no longer runs a public relations arm of its company, so there’s nobody to ask.

We asked peak Victorian motoring body, the VACC, what they thought about the insurance situation and VACC boss Geoff Gwilym claims more needs to be done by the insurance council.

“There is a significant labour shortage in the automotive industry, and it is getting worse,” Gwilym said.

“If the Insurance Council of Australia wants more people repairing vehicles, then what are they doing about it. What are they doing to attract more people into the industry? What are they doing about training? How about they use some of their significant profits to encourage people into the industry, instead of penalising motorists with high insurance premiums.”

“There are plenty of trained people ready and willing to repair EVs, but some EV companies will not make their parts available to the aftermarket industry,” he said.

Either way, if you are about to head out and buy a Tesla, or any other electric car for that matter, make sure you can get insurance first, otherwise you may end up with a nasty premium.

Go deeper on the cars in our Showroom, compare your options, or see what a great deal looks like with help from our New Car Specialists.

Paul Maric is a CarExpert co-founder and YouTube host, combining engineering expertise with two decades in automotive journalism.

James Wong

56 Minutes Ago

Damion Smy

7 Hours Ago

William Stopford

8 Hours Ago

William Stopford

12 Hours Ago

Damion Smy

13 Hours Ago

William Stopford

13 Hours Ago

Add CarExpert as a Preferred Source on Google so your search results prioritise writing by actual experts, not AI.