William Stopford

2026 Skoda Enyaq RS priced: Updated sporty electric SUV cheaper than before

The hottest version of the mid-size Skoda Enyaq electric SUV has been updated with sleeker looks and more equipment, for a lower list price.

46 Minutes Ago

We look at how the increasing price of crude oil affects the price you pay at the petrol pump as the war in the middle east rages on.

Publisher

Publisher

Every time oil charges towards US$100 a barrel, the same question comes back: if a barrel is only 158.987 litres, why are Australians paying well over $2.00 a litre at the pump? As of today’s date, Brent crude settled at US$100.21 a barrel.

At exactly US$100 a barrel, the crude itself works out to 62.9 US cents per raw litre. Using the Reserve Bank’s current AUD/USD rate of 0.70, that converts to A$142.71 a barrel, or 89.8 Australian cents per litre before refining, freight, storage, wholesaling, retailing or tax.

If you use the actual Brent close of US$100.21 rather than the round-number scenario, the raw crude cost is roughly 63.0 US cents a litre or 90.0 Australian cents a litre.

That barrel-to-bowser maths is a useful hook, but it breaks almost immediately in the real world. Australia is effectively a price taker in refined fuel. The Australian Institute of Petroleum (AIP) says local petrol pricing is driven by Singapore Mogas 95, diesel is driven by Singapore Gasoil 10ppm sulfur, and there is usually a one to two week lag before moves in those regional benchmarks show up in Australian wholesale prices.

It also matters that Australia now has only two operating refineries left: Ampol’s Lytton refinery in Queensland and Viva Energy’s Geelong refinery in Victoria. That means the local market is still heavily exposed to imported refined product pricing, even before you get to transport, terminal and retail costs.

| Item | Value |

|---|---|

| Brent scenario | US$100.00/bbl |

| Standard oil barrel | 158.987L |

| US$100 crude only | 62.9 US cpl |

| Actual Brent close converted at AUD/USD 0.7007 | A$143.01/bbl |

| Actual Brent close in A$ terms | 90.0 cpl |

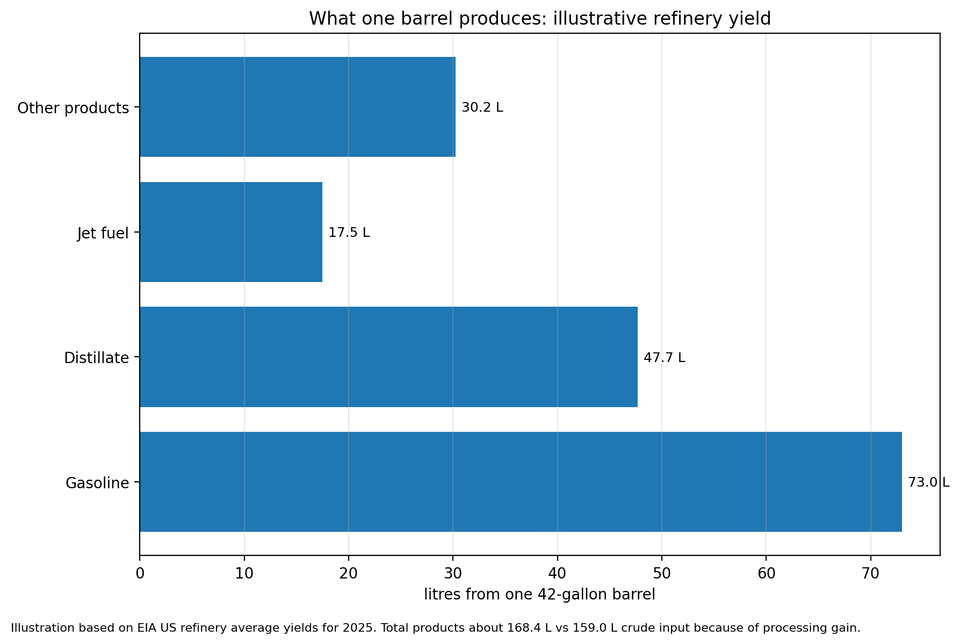

The first mistake in this debate is treating crude oil as if it turns straight into the same volume of petrol. It does not. A refinery splits a barrel into a range of products including petrol, diesel, jet fuel, LPG, petrochemical feedstocks, asphalt and other outputs. Total product output can even end up larger than the original input volume because of processing gain.

Using the latest US refinery yield data as a clean illustration, the 2025 average barrel produced 45.9 per cent finished motor gasoline, 30.0 per cent distillate fuel oil and 11.0 per cent kerosene-type jet fuel, with total product output equivalent to 105.9 per cent of the original barrel. On a 158.987-litre basis, that works out to roughly 73.0 litres of petrol-like product, 47.7 litres of distillate and 17.5 litres of jet fuel, with the balance made up by other products and processing gain.

That is not an Australia-specific refinery recipe, but the local direction is similar. Ampol says Lytton’s 2025 production slate was 43 per cent petrol, 48 per cent middle distillates and 9 per cent other products. So even locally, the barrel is being split across multiple fuel streams rather than becoming a neat line of petrol litres.

| Product from one barrel | Yield | Approx. litres |

|---|---|---|

| Finished motor gasoline | 45.9% | 73.0L |

| Distillate fuel oil | 30.0% | 47.7L |

| Kerosene-type jet fuel | 11.0% | 17.5L |

| Other products plus processing gain | 19.0% | 30.2L |

| Total refined products | 105.9% | 168.4L |

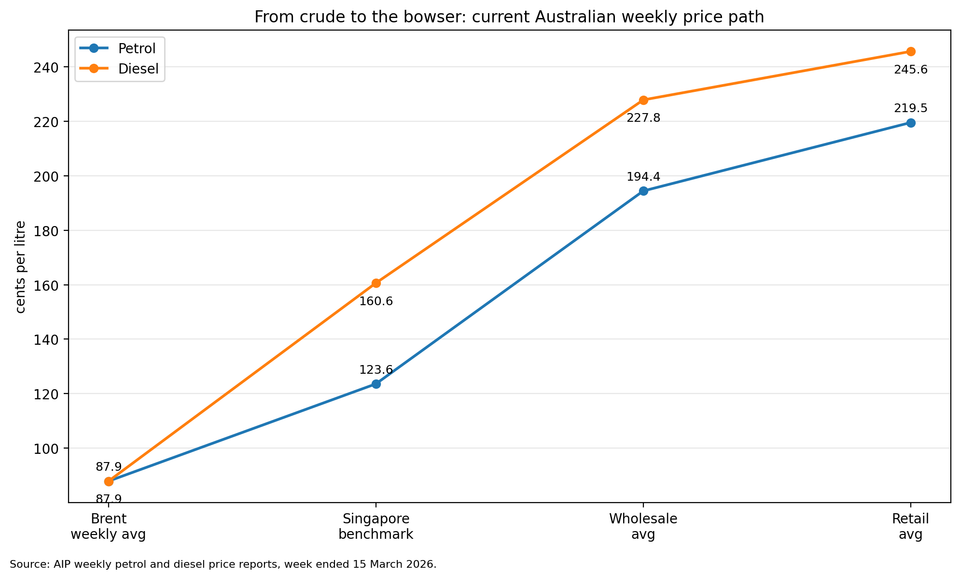

The best way to explain what motorists pay is to follow the current price stack rather than jump straight from crude to the pump. In the latest AIP weekly data, national average petrol was 219.5cpl and diesel was 245.6cpl for the week ended 15 March 2026.

Wholesale averages were 194.4cpl for petrol and 227.8cpl for diesel. The same AIP reports showed Brent at 87.9 Australian cents per litre equivalent, Singapore Mogas 95 at 123.6cpl and Singapore Gasoil 10ppm at 160.6cpl.

For petrol, that means the move from Brent to the Singapore petrol benchmark was 35.7cpl. The step from Mogas 95 to average Australian wholesale petrol was another 70.8cpl. The step from wholesale to retail was 25.1cpl. For diesel, the jump from Brent to Singapore Gasoil was a much larger 72.7cpl, then another 67.2cpl to wholesale and 17.8cpl from wholesale to retail. Diesel was 26.1cpl dearer than petrol in the latest national averages. Those are gross pricing steps, not neat profit lines.

AIP is explicit on that point. For petrol, it says Mogas 95, shipping and taxes make up almost the entire wholesale price, and it separately notes that landed costs and margins include quality premiums, insurance and loss, wharfage, terminal operating costs, administration, marketing and corporate and government charges. It makes the same point on diesel. At the retail end, AIP says the retail-wholesale gap still has to cover land transport, administration, marketing, wages, rent and utilities.

| Fuel | Stage | Price (cpl) | Move from previous stage |

|---|---|---|---|

| Petrol | Brent crude equivalent | 87.9 | — |

| Petrol | Singapore Mogas 95 | 123.6 | +35.7 |

| Petrol | Australian wholesale average | 194.4 | +70.8 |

| Petrol | Australian retail average | 219.5 | +25.1 |

| Diesel | Brent crude equivalent | 87.9 | — |

| Diesel | Singapore Gasoil 10ppm | 160.6 | +72.7 |

| Diesel | Australian wholesale average | 227.8 | +67.2 |

| Diesel | Australian retail average | 245.6 | +17.8 |

These are the latest AIP weekly averages, with Brent/Mogas/Gasoil based on the week to Friday 13 March 2026 and retail/wholesale averages published for the week ended 15 March 2026. The one-to-two-week lag from Singapore pricing into Australian wholesale prices is also from AIP.

Tax is one of the cleanest parts of the fuel stack because it is published and formula-driven. The ATO updated excise duty rates from 3 February 2026, lifting both petrol and diesel excise to 52.6 cents per litre. GST remains 10 per cent.

At the latest national average petrol price of 219.5cpl, GST works out to 19.95cpl. Add 52.6cpl in excise and total government take is 72.55cpl. That means about 33.1 per cent of the average petrol price is tax, leaving about 146.95cpl to cover everything else.

At the latest national average diesel price of 245.6cpl, GST works out to 22.33cpl. Add the same 52.6cpl excise and total government take is 74.93cpl. That is about 30.5 per cent of the pump price, leaving roughly 170.67cpl for the non-tax stack.

| Fuel | Retail price (cpl) | Excise (cpl) | GST (cpl) | Total government take (cpl) | Government share |

|---|---|---|---|---|---|

| Petrol | 219.5 | 52.6 | 19.95 | 72.55 | 33.1% |

| Diesel | 245.6 | 52.6 | 22.33 | 74.93 | 30.5% |

Calculations use the AIP national average retail prices and the ATO’s current excise and GST guidance.

The ACCC publishes the clearest public breakdown of retail petrol pricing in Australia, and it is very careful with terminology. In the December quarter of 2025, average petrol across the five largest cities was 180.4cpl. The ACCC attributed 76.1cpl to Mogas 95, 20.0cpl to other wholesale costs and margins, 66.4cpl to excise and wholesale GST, and 17.9cpl to what it calls the gross indicative retail difference.

That last number is not net profit. The ACCC says the gross indicative retail difference is a broad indicator of gross retail margins because it includes both retail operating costs and profits. It also notes that prices, costs and profits vary significantly between sites, and that timing differences between wholesale and retail prices can move the figure around. In other words, it is a very useful indicator, but it is not a clean bowser-profit number.

For broader context, the ACCC said the annual average gross indicative retail difference in calendar 2025 was 16.3cpl, just 0.2cpl above the inflation-adjusted 10-year average. That is a good reminder that a scary headline pump price does not automatically mean retailers are suddenly minting money on every litre.

| Component | cpl | Share of 180.4cpl retail price |

|---|---|---|

| Mogas 95 | 76.1 | 42.2% |

| Other wholesale costs and margins | 20.0 | 11.1% |

| Excise and wholesale GST | 66.4 | 36.8% |

| Gross indicative retail difference | 17.9 | 9.9% |

| Total retail petrol price | 180.4 | 100.0% |

Important nuance: the ACCC’s bar chart sums to 180.4cpl using 66.4cpl for excise and wholesale GST. The watchdog separately notes that total excise and GST was 68.0cpl once retail GST is included.

If you go looking for a neat public number for the operating margin of “BP or Shell” in Australia, you hit a wall quickly. BP reported underlying replacement cost profit of US$7.5 billion for 2025 at a group level, while Shell reported Products adjusted earnings of US$2.177 billion. Those are real numbers, but they are global or segment-level disclosures, not a clean Australian cents-per-litre bowser margin. In Australia, Shell-branded fuels are supplied under licence by Viva Energy.

The more useful local public filings are Ampol and Viva Energy, because they show what downstream businesses earn in Australia, but even then you have to separate retail earnings from refining margin, and fuel margin from convenience-store economics. Ampol’s figures include combined fuel and shop margin in its convenience retail business. Viva Energy’s figures do the same, while also separately disclosing Geelong refining performance. None of those numbers is a direct substitute for a pure “profit per litre at the pump” figure.

| Company | Metric | FY2025 value | Why it matters |

|---|---|---|---|

| Ampol | Convenience retail sales volumes | 3.49 BL | Shows the scale of retail fuel sales |

| Ampol | Fuel and shop margin excl site costs | $1,244.2m | Gross margin before site costs |

| Ampol | Site costs | $383.1m | Cost of running the retail network |

| Ampol | Fuel and shop margin | $861.2m | After site costs, before broader overheads |

| Ampol | Convenience Retail EBIT | $373.7m | Segment earnings, not pure fuel margin |

| Ampol | Lytton Refiner Margin | US$10.34/bbl | Refinery economics, not retail margin |

| Ampol | Lytton EBITDA | $226.9m | Refining earnings |

| Viva Energy | Fuel sales | 5,146 ML | Scale of fuel sold |

| Viva Energy | Fuel and shop margin | $1,633m | Combined gross margin |

| Viva Energy | Convenience & Mobility EBIT (RC) | $61.9m | Retail-focused earnings |

| Viva Energy | Geelong refining margin | US$9.61/bbl | Refinery economics |

| Viva Energy | Refining EBITDA (RC) | $93.0m | Geelong refining earnings |

| Viva Energy | Refining EBITDA after operating costs | A$2.5/bbl | Approximate post-cost per-barrel result |

These are the local public numbers that are most relevant but while they are useful context, they are not direct Australian pump-margin disclosures.

Ampol’s Lytton disclosure is especially useful because it shows how a refinery margin is built. In 2025 it comprised a Singapore weighted average margin of US$13.54 a barrel, plus product freight of US$5.50 and a quality premium of US$1.04, offset by a landed crude premium of US$7.55, yield loss of US$0.97 and other related hydrocarbon costs of US$1.21. That produced the reported Lytton Refiner Margin of US$10.34 a barrel. Again, that is a refining number, not a bowser-profit number.

Viva Energy tells a similar story from the Geelong side. It reported a Geelong refining margin of US$9.61 a barrel in FY2025. But once energy, operating, supply and corporate costs were absorbed, refining EBITDA was A$93.0 million, which the company equated to about A$2.5 a barrel. That is a handy reality check on the difference between gross refining margin and the actual earnings that fall out the bottom.

Diesel does not behave like petrol in Australia. AIP says there is no retail discounting cycle for diesel because only about 25 per cent of diesel is sold through retail outlets, much of that retail volume is sold through contracts or fuel cards, and most diesel is sold in bulk on longer-term contracts.

That helps explain why diesel can stay materially dearer than petrol for long periods even though both ultimately start from the same crude oil pool. In the latest national averages, diesel was 245.6cpl against 219.5cpl for petrol — a 26.1cpl premium.

So if you have ever wondered what a round-number US$100 barrel means for Australia, you may not have a slightly better idea (or you may be even more confused).

At about 62.9 US cents or 89.8 Australian cents per raw litre on today’s prices, the war in the middle east is having a significant impact on the prices Australians are paying at the pump and while Australians obviously do not buy raw litres of crude, they buy refined petrol and diesel priced off Singapore product benchmarks, moved through terminals and service stations, and loaded with excise and GST.

The latest Australian numbers make that obvious. Petrol moves from a Brent equivalent of 87.9cpl to Singapore Mogas 95 at 123.6cpl, then to average wholesale petrol at 194.4cpl and average retail petrol at 219.5cpl. Diesel starts at the same 87.9cpl crude reference, jumps to Singapore Gasoil at 160.6cpl, then to wholesale diesel at 227.8cpl and retail diesel at 245.6cpl.

Government takes a big slice (surprise!) and at the latest averages, tax is about 72.6cpl on petrol and 74.9cpl on diesel. Everything else has to cover the refined product benchmark, shipping, import costs, terminal costs, wholesaling, transport to site, wages, rent, electricity and only then whatever profit is left.

Sources: Reuters Brent close, RBA AUD/USD, ACCC, AIP, public financial reports.

Alborz Fallah is a CarExpert co-founder and industry leader shaping digital automotive media with a unique mix of tech and car expertise.

William Stopford

46 Minutes Ago

Matthew Hansen

2 Hours Ago

William Stopford

3 Hours Ago

Marton Pettendy

4 Hours Ago

Dave Kavermann

5 Hours Ago

James Wong

7 Hours Ago

Add CarExpert as a Preferred Source on Google so your search results prioritise writing by actual experts, not AI.